Quiet Capital Destruction

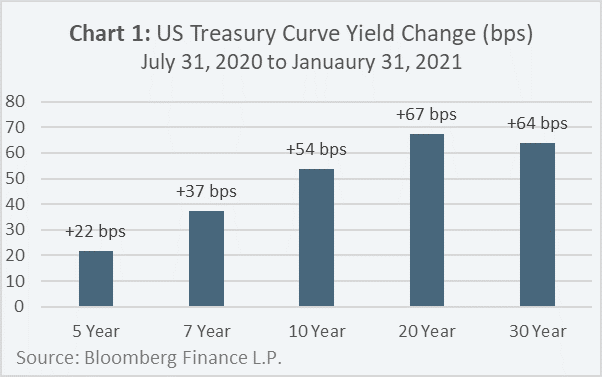

Over the past six months, the US bond market1 has been losing money. As illustrated in Chart 1, longer-term US interest rates rose anywhere between 22 bps and 67 bps between July 31, 2020 and January 31, 2021, and the US bond market posted a cumulative price return of -2.0% while posting negative monthly price returns in five of the six months.

After a year like 2020, where the US bond market posted a calendar year total return of 7.6%, the negative price volatility of the past six months might come as a sobering reality to some who have come to the realization that investors could potentially lose money in their bond portfolios in 2021 and beyond!

Under the Hood of Nominal Interest Rates

The recent losses in the US bond market can be traced to one of the classic bond market risks – interest rate risk. To help give context to what might be driving the rise in interest rates, it helps to decompose long-term nominal interest rates into the sum of their parts, which are generally:

- inflation premium;

- real interest rate;

- term premium.

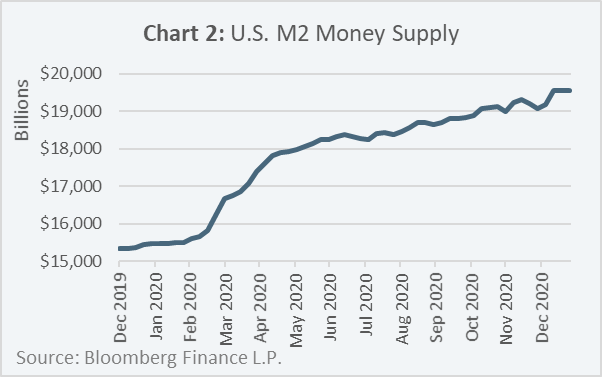

Proponents of the Quantity Theory of Money2 would argue that the increase in interest rates is a direct result of the increase in the US money supply (Chart 2), which in 2020 alone rose by over US$4 trillion due to the fiscal and monetary stimulus programs initiated to combat the COVID-19 pandemic.

With further fiscal stimulus measures being debated by the US government and the Federal Reserve continuing their monetary stimulus programs, investors may very well be concerned about higher future inflation impacting higher interest rates, and a solution that may naturally attract investors are Treasury Inflation Protected Securities (“TIPS”).

Tipping points for TIPS

TIPS are US Treasuries that incorporate a principal adjustment factor based on the change in the US Urban Consumers Consumer Price Index Non-Seasonally Adjusted (“CPI”). The principal adjustment factor impacts TIPS in two ways:

1) at maturity, the par value paid back to the investor is based on the initial par value of the TIPS multiplied by the principal adjustment factor;

2) the semi-annual coupon payment is based on the fixed coupon rate multiplied by the adjusted principal amount.

The result is that investors receive an inflation-adjusted, or “real” yield by holding a TIPS to maturity, no matter what level of inflation is realized over the bond’s term. This differs from a nominal US Treasury where the yield premium to compensate investors for future inflation is embedded in its yield-to-maturity at the time of purchase, which may not match the level of realized inflation over the bond’s term – this embedded inflation premium in nominal Treasuries is why they have higher coupon rates than comparable maturity TIPS.

TIPS are certainly an effective solution for investors looking to protect their bond portfolios against inflation, however it is important for investors to make the distinction between whether they want to protect against inflation or rising interest rates.

Before investing in TIPS, it could be helpful if investors consider the following points:

TIPS protect investors from inflation, not from rising interest rates

It is easy to conflate these points, as they are sometimes viewed as being one and the same, however consider the general composition of nominal interest rates mentioned earlier in the paper – inflation premium, real interest rate and term premium. TIPS protect investors from realized inflation over a bond’s term, however TIPS also have price sensitivity to changes in real interest rates and term premiums.

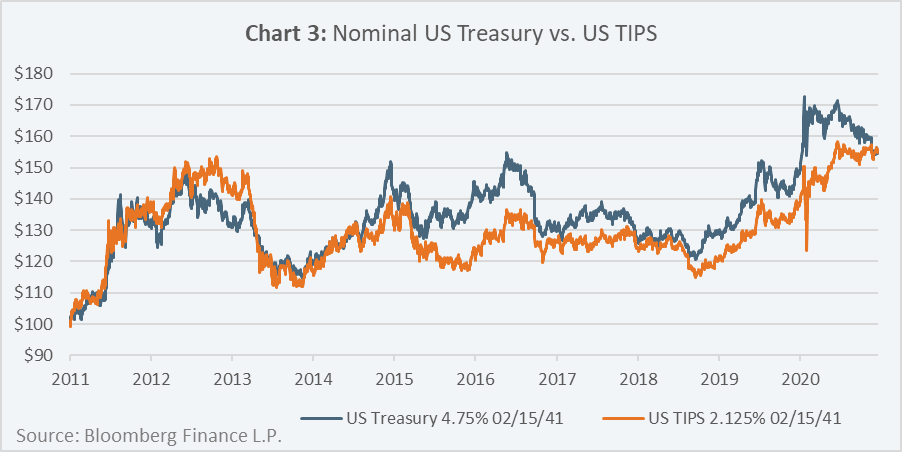

For more context, consider Chart 3, which compares the prices of a similar maturity nominal US Treasury and US TIPS. One key takeaway is that over the past 10-years, based on daily price changes, the correlation of the two bond prices has been 0.83. Another takeaway is that between May 2, 2013 and September 5, 2013, during the infamous “Taper Tantrum”, the TIPS bond price depreciated by 23.7%!

Changing inflation expectations could more than offset the actual inflation compensation

In addition to compensating investors for changes in realized CPI inflation, through the principal adjustment factor, TIPS prices can also change based on changes to the market’s perception of future inflation prior to the bond’s maturity.This means that TIPS prices may increase in response to higher inflation expectations and decrease in response to lower inflation expectations.

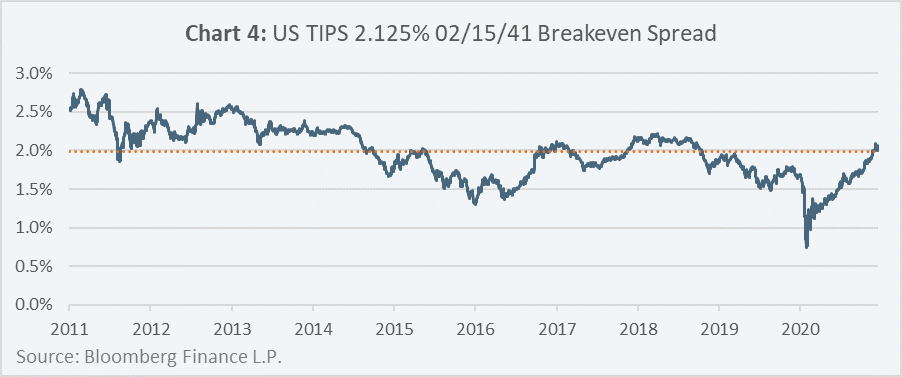

The market expectation of future inflation is reflected in the TIPS breakeven spread, which is simply the difference between a similar maturity nominal Treasury yield and TIPS yield (Chart 4).

Simply put, the TIPS breakeven spread is the average level of future inflation that makes an investor indifferent between holding to maturity a nominal Treasury or a TIPS with similar maturity dates.

The TIPS breakeven spread is a helpful metric to determine the relative attractiveness of a nominal Treasury and a TIPS, as it can also be interpreted as the amount of inflation premium embedded in the nominal Treasury. If you think future inflation will be greater than the TIPS breakeven spread, you might find there is more value in the TIPS; if you think future inflation will be less than the TIPS breakeven spread, you might find there is more value in the nominal Treasury.

Corporate Floating Rate Notes (“FRNs”) may offer protection against rising interest rates with less volatility

In Canada, the coupon payments for corporate FRNs are based on a reference rate known as the Canadian Dollar Offered Rate (“CDOR”), which is derived from Bankers’ Acceptance yields. In addition to the CDOR yield, Canadian corporate FRNs also pay a fixed spread above CDOR which is determined at the time of the FRN issuance. As the CDOR yield is based on short-term interest rates, it tends to remain relatively constant over longer periods of time and generally makes significant adjustments when the Bank of Canada (“BoC”) adjusts the overnight policy rate.

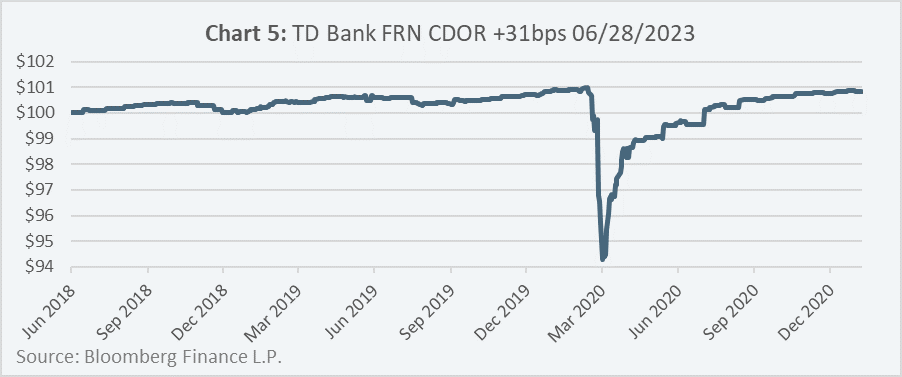

As corporate FRN coupons adjust to changes in short-term interest rates, their price sensitivity to interest rate changes (duration) is typically very low. While corporate FRN prices may still react to changes in the market’s perception of their credit quality, the prices of higher quality corporate FRNs (such as the TD Bank FRN covered bond3 in Chart 5) have shown to be generally stable over time.

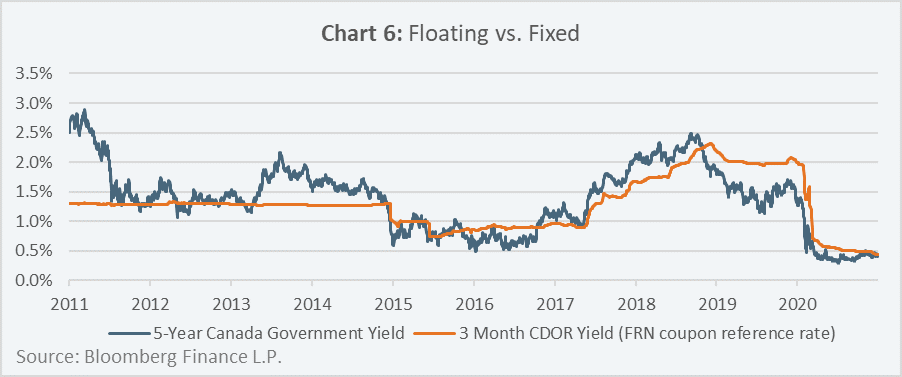

An important connection to make with respect to FRNs being an alternative to TIPS is that while FRN coupons do not directly adjust to changes in CPI, the BoC overnight policy rate is heavily influenced by the level of inflation. In an environment of rising inflation, it is likely the BoC would respond by increasing the overnight policy rate, thus increasing the FRN coupon income. Another attractive dynamic to Canadian FRNs is that at certain times in the past 10-years (as illustrated in Chart 6) the yield of CDOR has been greater than the yield of a 5-year Government of Canada yield. When this happens, it means that FRNs offer more yield and less exposure to interest rate risk compared to the 5-year Government of Canada bond.

Final Thoughts

With interest rates on the rise and further monetary and fiscal stimulus measures stoking expectations for higher future inflation, bond investors should rightly be taking stock of their exposure to interest rate risk in their bond portfolios.

While TIPS may be viewed as an effective solution to the rising interest rate challenge, it is important to remember that TIPS only solve one piece of the rising interest rate puzzle, and they do not protect against rising real interest rates or rising term premium. Real GDP growth is generally a driving factor behind real interest rates, and one potential negative scenario for TIPS is a post-COVID economic recovery that might cause real interest rates to rise and TIPS prices to fall.

Another risk factor for TIPS is changing expectations for future levels of inflation. Given the recent increase in the TIPS breakeven spread (Chart 4) and now that it is near its long-term average of 2%, which is also the target inflation rate set by the Fed, it seems less likely this factor will drive meaningful value to TIPS investors going forward.

Corporate FRNs provide a more comprehensive solution to investors wanting to protect their bond portfolios from rising nominal interest rates and not just rising inflation. FRNs also provide more optionality to capture additional yield by diversifying into different levels of the credit quality spectrum. Making investments in lower credit quality FRNs does increase credit risk however, which can be mitigated through prudent credit analysis.

The ultimate decision of whether to invest in TIPS, nominal Treasuries or FRNs, however, depends on the unique circumstances of the individual investor. Consultation with a professional financial advisor can be a helpful tool for investors wanting to tailor personal asset mixes that meet their needs.

1 US bond market is represented by the ICE BofAML US Broad Market Index

2 The formula for the Quantity Theory of Money (per Investopedia) is: MV = PT, where M = money supply, V = velocity of money, P = average price level, T = volume of transactions in the economy

3 Covered Bonds are bond that are typically issued by banks where the borrower has security not just against the issuer but by an additional pool of high-quality mortgages that are separate from the bank’s balance sheet. Covered bonds typically have credit ratings of AAA.