Revisiting LRCNs

In our September 2020 commentary titled A New Type of Security is Shaking Up the Canadian Preferred Share Market, we discussed the introduction of Limited Recourse Capital Notes (“LRCNs”) to the Canadian marketplace and how these securities were disrupting the issuance of new preferred shares by the Big-6 Canadian banks1. In our closing remarks we mentioned:

“While LRCN/AT1 issuances in Canada have been solely made by the Big-6, it is possible that other players in the Canadian preferred share market will follow-suit given the issuer tax benefits of LRCNs/AT1s over preferred shares.”

Since then, new issuance of LRCNs totalled $3.775 billion through March 2021, with over half of that from non-Big-6 Canadian bank issuers such as Manulife Financial Corp., Empire Life Insurance Company and Canadian Western Bank.

The Rotation Trade

LRCNs are almost perfect substitutes for fixed- reset preferred shares as they share the same coupon2 reset feature, where every five years the coupon resets based on the prevailing level of the 5-year Canada bond yield plus a fixed yield spread, also known as a “reset-spread”. Furthermore, LRCNs offer a relative tax advantage to their holders compared to preferred shares via a mechanism known as the “tax shield”.

As companies generally have a mandate to maximize shareholder value, it is a no-brainer that companies would want to call their fixed-reset preferred shares – which on a par-value basis makes up approximately $56 billion (or approximately 80%) of the S&P/TSX Preferred Share Index – as soon as they could to reissue them as LRCNs. For investors, this potential issuer rotation from preferred shares into LRCNs represents an opportunity to realize capital gains by purchasing fixed-reset preferred shares trading at discounts with the expectation they will eventually be called by their issuers at par.

This LRCN rotation is not a foregone conclusion however, because as it stands today it would not necessarily maximize shareholder value for all fixed-reset preferred shares to immediately be called. To get a better sense of which preferred shares are more likely to be called in the near-term, it is helpful to analyze the relative cost of fixed-reset preferred shares and LRCNs from the perspective of the issuer. Given the similar coupon structures of the two securities, this can be done by comparing the reset spreads of LRCNs, adjusted for the tax shield benefit, to the reset spreads of fixed-reset preferred shares.

LRCN Tax-Adjusted Reset Spread

It is important to remember that the level of reset spread for LRCNs and fixed-reset preferred shares reflects the market’s sentiment of risk for the issuer of the security at the time of issuance and the reset spread remains fixed throughout the term of the security – a greater spread generally indicates more risk, and a smaller spread generally indicates less risk.

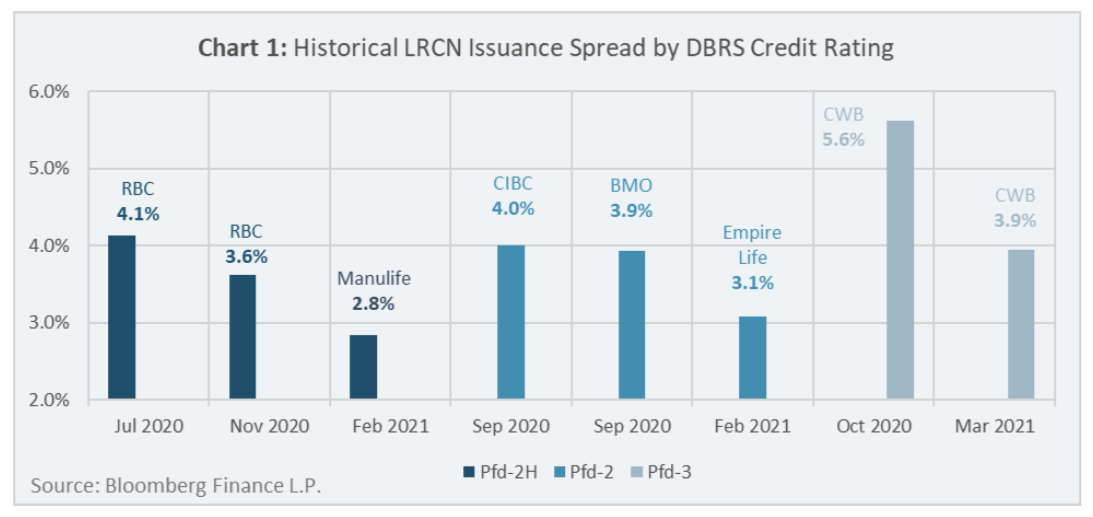

To determine the general prevailing level of LRCN reset spreads, we have used a recent transactions approach from past LRCN issuances and grouped them by common issuer DBRS credit ratings. As indicated in Chart 1, the most recent LRCN reset spreads were 2.8%, 3.1% and 3.9%, for issuers with DBRS credit ratings of Pfd-2H, Pfd-2 and Pfd-3, respectively.

To analyze the relative value between LRCNs and fixed-reset preferred shares on an apples-to- apples basis, the issuer benefits from the tax shield must also be taken into consideration and is reflected in a metric which we will call the “tax- adjusted reset spread”3. On that basis, the tax- shield adjusted LRCN reset spreads are determined to be 2.4%, 2.5% and 3.6%, for issuers with DBRS credit ratings of Pfd-2H, Pfd-2 and Pfd-3, respectively.

Fixed-Reset Preferred Share Reset Spread

With the tax-adjusted reset spreads for LRCNs estimated, the decision for issuers of fixed-reset preferred shares to either rotate, or not, into LRCNs is a simple question of what has the lower reset spread – the LRCN tax-adjusted reset spread or the fixed-reset preferred share reset spread?

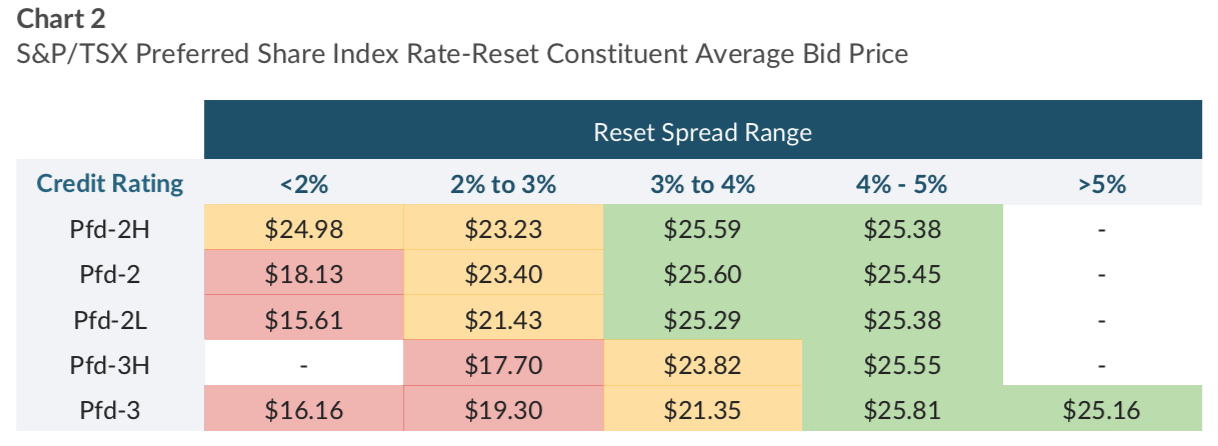

The market pricing of preferred shares seems to confirm the validity of this question. Chart 2 shows a matrix of average fixed-reset preferred share prices based on reset spread ranges and issuer DBRS credit quality categories – values shaded in green indicate an average bid price above par; values shaded in orange, an average bid price within a 20% discount to par; values shaded in red, an average bid price greater than a 20% discount to par.

How to Position for a Continued LRCN Rotation Trade

Given an estimated tax-adjusted reset spread of 3.6% for the lowest issuer credit quality category (Pfd-3), it makes sense that all preferred shares with reset spreads greater than 4% are on average trading at a premium, as the market is likely pricing-in that these securities could be called by their issuers at par.

The potential for capital gain opportunities by virtue of other discounted preferred shares being called by their issuers might likely be determined by the future level of LRCN tax-adjusted reset spreads relative to fixed-reset preferred share reset spreads of similar credit qualities. It is important to remember that LRCN reset spreads can change depending on market sentiment, while reset spreads for preferred shares are fixed. For example, if LRCN tax-adjusted reset spreads with credit ratings of Pfd-2H, Pfd-2 and Pfd-2L were to at most narrow to 2%, we could expect orange category preferred share prices in the 2% to 3% column to be called at par, which could result in an average capital gain of approximately 10% for those preferred shares (based on recent prices).

Red category preferred share prices from Chart 2 are those with very low reset spreads – and well below the current estimated levels of LRCN tax- adjusted reset spreads. Their significant price discounts to par are justified as it would require the market to significantly reduce the levels of LRCN reset spreads before it would represent good value for issuers to call those preferred shares.

LRCN Rotation Timing

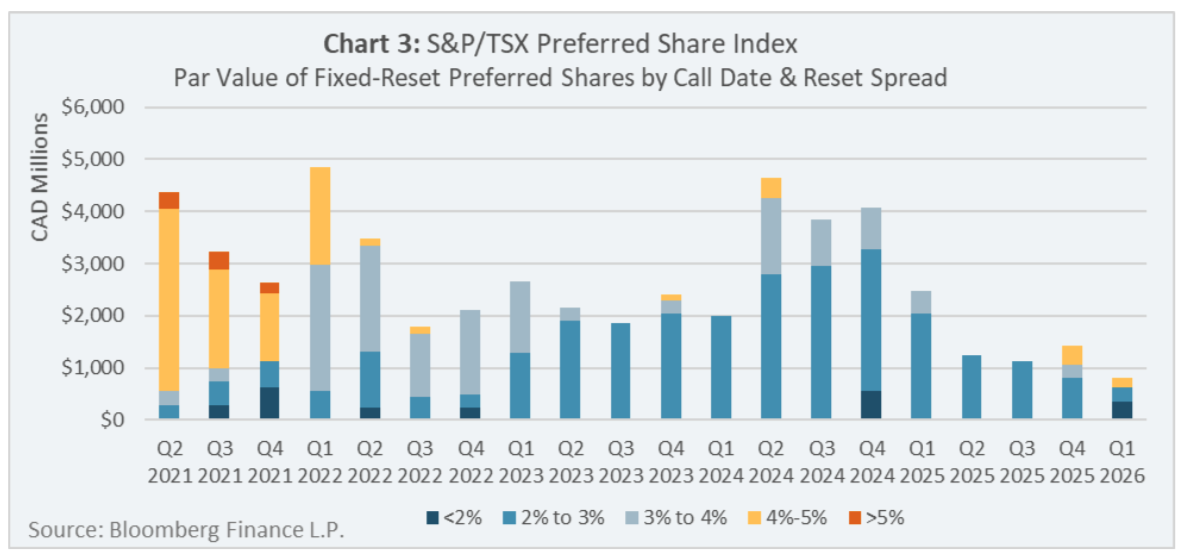

As fixed-reset preferred shares have scheduled call dates every five years from the time they are issued, it gives a specific date that a potential rotation from preferred shares to LRCNs might take place.

As illustrated in Chart 3, a significant amount of fixed-reset preferred shares with reset spreads greater than 4% – a total of $9.4 billion in par value – have their scheduled call dates coming up over the next four quarters. Preferred shares with reset spreads in the 3% to 4% category – a total of $9.1 billion in par value – have their call dates coming up over the next eight quarters.

Conclusion

Given the similar coupon structure and relative tax advantage of LRCNs compared to preferred shares, the continued issuance of LRCNs is likely to continue in the months and years to come.

There are at least three key factors that could affect the speed at which this LRCN rotation takes place:

- LRCN tax-adjusted reset spreads;

- Fixed-reset preferred share reset spreads;

- The schedule of call dates for specific preferred share issues.

As a general rule, if credit conditions continue to improve it could likely support an acceleration of LRCN issuance, which could potentially accelerate future opportunities for investors to benefit from discounted preferred shares being called at par.

For ordinary investors, investing in the Canadian preferred share market can be tricky due to the generally low supply of issues on exchanges and high commissions charged by dealers to trade them. That is why investors might find value in an actively managed preferred share solution such as a mutual fund or an ETF.

Lysander Funds Limited offers two preferred share funds to investors, Lysander-Slater Preferred Share Dividend Fund and Lysander-Slater Preferred Share ActivETF.

1 “Big-6 Canadian Banks” include: Bank of Montreal, Bank of Nova Scotia, Canadian Imperial Bank of Commerce, National Bank, Royal Bank of Canada and Toronto-Dominion Bank.

2 The term “coupon” is used to describe both the traditional coupon of the LRCN and the dividend payment of the preferred share.

3 The tax-adjusted reset spreads were calculated by multiplying the most recent LRCN issuance spreads by DBRS credit rating category by 1 minus the average tax rate for issuers of preferred shares in the same DBRS credit rating category.