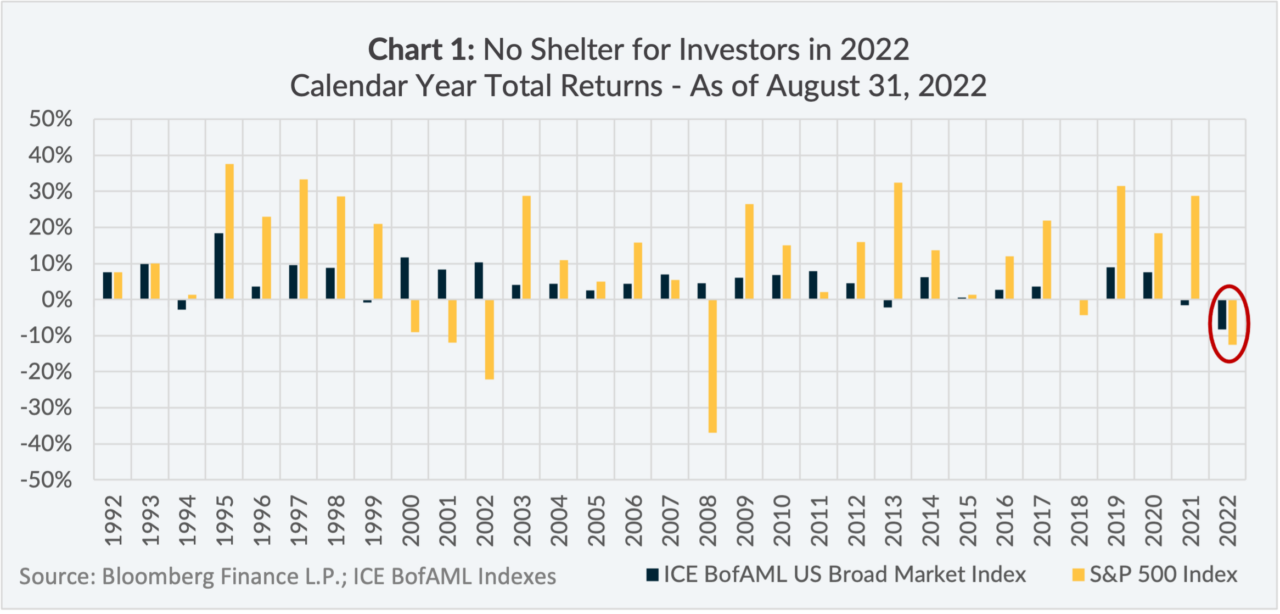

No shelter for investors in 2022

2022 has been a challenging year for investors. Not just for high-risk equity investors, but also for low-risk bond investors. As illustrated in Chart 1, year-to-date as of August 31, 2022, the S&P 500 Index (“US equities”) and the ICE BofAML US Broad Market Index (“US bonds”) declined in tandem for the first time in over 30-years.

This is not supposed to happen, according to generally accepted investment theory. Bonds are meant to soften the blow of poor performance during periods when equity markets decline.

Many investors are rightly concerned with the correlated selloff of US equities and bonds; however, others are finding that now is a time to be optimistic. As the saying goes: “a market is made up of buyers and sellers” – the buyers being “bulls” and the sellers being “bears”.

When faced with periods of uncertainty, investors naturally look to the past to try and glean patterns that could be used to infer the future. Today the case is no different, as it appears market bulls and bears have both seized on different past environments to support their views going forward.

BULLS AND BEARS

At a high-level, the bull-camp and bear-camp narratives driving markets in 2022 could be described as follows:

Bull-Camp Narrative: 2019 “Powell Pivot”

The current environment will be reminiscent of the period in late-2018/early-2019 when the Federal Reserve was raising the overnight rate in response to rising inflation, then pausing in response to US equity market weakness.

The general inference for 2022 is inflation will resolve itself over time given the overnight rate increases that have already taken place, and the Federal Reserve will respond to declining inflation by lowering the overnight rate.

The generally expected result is an upward movement for both US equities and bonds.

Bear-Camp Narrative: Volker’s 1970s

The current environment will be reminiscent of the period in the 1970s when there was high inflation and then-Fed Chairman, Paul Volker, aggressively raised the overnight rate to cool inflation.

The general inference for 2022 is inflation will remain more persistent, and the Federal Reserve will need to continue a path of overnight rate increases. Term interest rates could also continue to rise if inflation expectations become entrenched amongst the public.

The generally expected result is continued downward pressure for both US equities and bonds.

BULLS AND BEARS IN ACTION

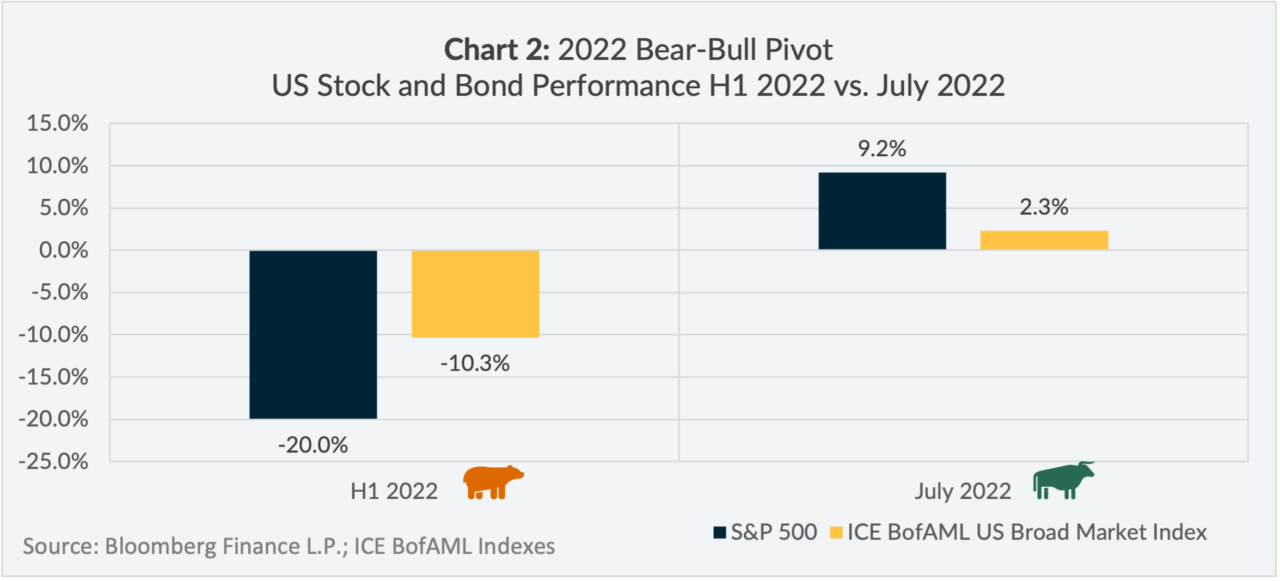

To see both bull-camp and bear-camp narratives in action, one must look no further than the 2022 intra-year performance of US stocks and bonds.

As illustrated in Chart 2, the first half of 2022 appeared to be dominated by the bear-camp narrative, with US equities and bonds declining in tandem. However, in July 2022, market sentiment seemed to shift to the bull-camp narrative, with both US equities and bonds gaining in tandem.

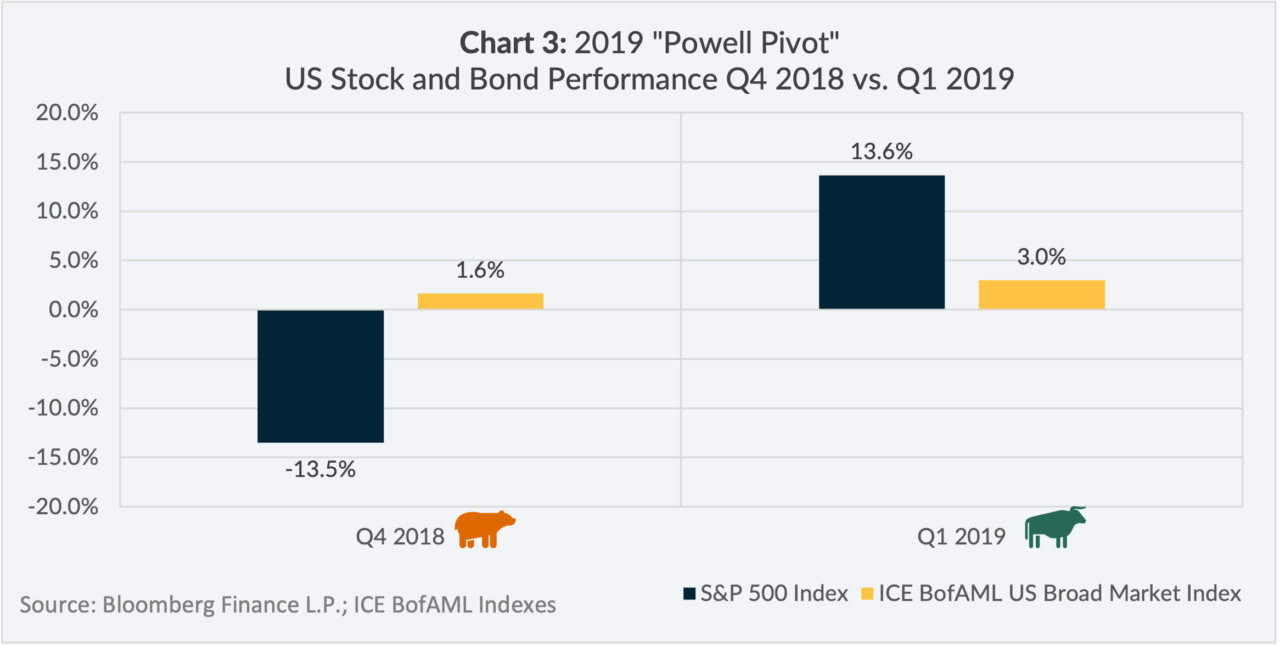

What is notable about the 2022 bear-bull market pivot, is its similarity to a pivot that took place in 2019.

As illustrated in Chart 3, US equities declined in Q4 2018 in response to the Federal Reserve increasing the overnight rate then. In January 2019, when the Federal Reserve announced it would pause increasing the overnight rate, US equities and bonds proceeded to rally in response to the more accommodative stance from the Federal Reserve.

THE INFLATION ELEPHANT IN THE ROOM

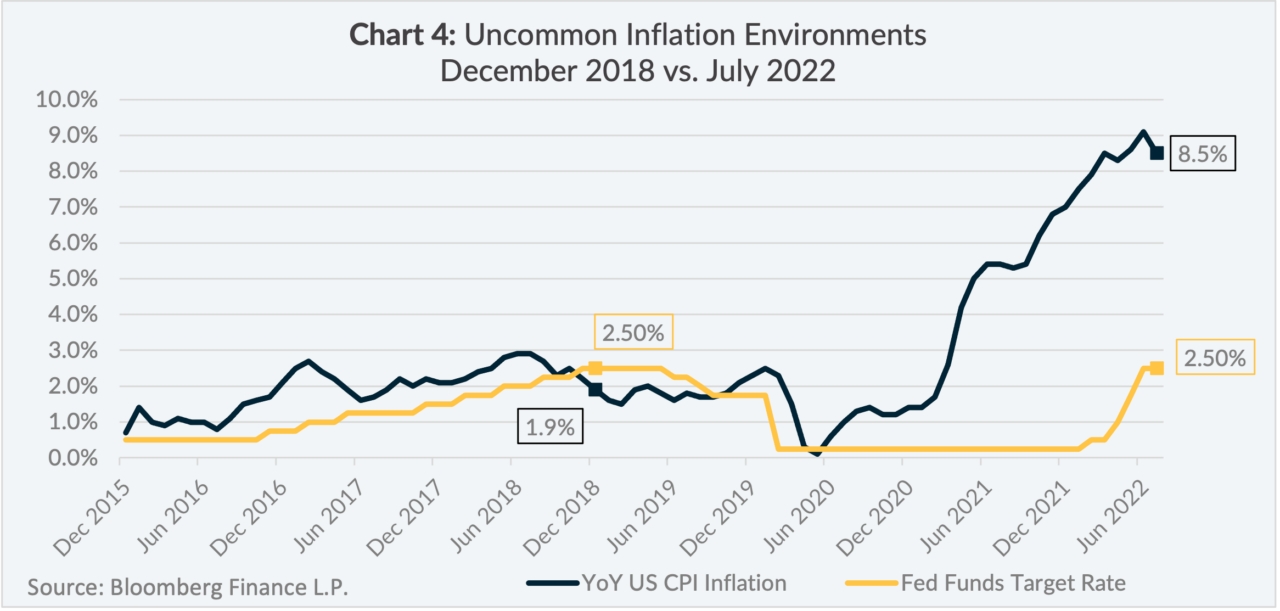

Given markets’ reaction in both 2022 and 2019, it is clear a common hinge on which market sentiment swings is the directionality of the overnight rate.

As illustrated in Chart 4, the overnight rate in July 2022 was at the same level when the Federal Reserve pivoted in 2019, except in July 2022, YoY US CPI was 8.5% vs. 1.9% in December 2018.

This was not lost on the Federal Reserve either, with the following except from the FOMC statement in January 2019:

IN SEARCH OF THE NEUTRAL OVERNIGHT RATE

The commitment from the Federal Reserve to cool inflation was most recently reinforced at the Federal Reserve Bank of Kansas City Economic Symposium at Jackson Hole, on August 26th, 2022. Federal Reserve Chairman, Jerome Powell, alluded to three important lessons:

- Central banks can and should take responsibility for delivering low and stable inflation.

- The public’s expectations about future inflation can play an important role in setting the path of inflation over time.

- We (the Federal Reserve) must keep at it until the job is done.

It is often said that to cool inflation the Federal Reserve needs to raise the overnight rate above its “neutral rate” – the rate at which it is neither stimulative or restrictive to an economy. The problem is the neutral rate is not explicity known, rather it is a rate based in theory.

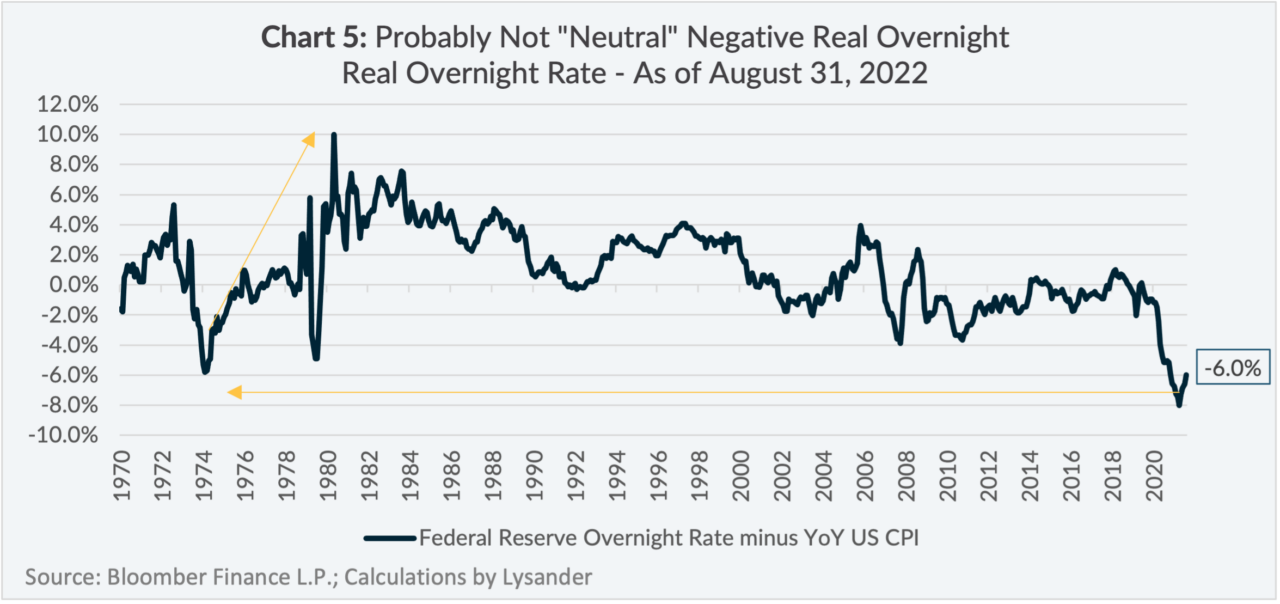

A metric that could be used as a proxy for the neutral rate is the real (after-inflation) overnight rate. As illustrated in Chart 5, the real overnight rate as of August 2022 was -6.0%, near its lowest reading since the initial inflation build-up of the early 1970s.

When Paul Volker was trying to cool inflation through the 1970s and 1980s, there was a noticable increase in the real overnight rate, with it peaking at a level 10.0% in early-1981.

While this may not give insight to an exact level for the neutral rate, it does suggest that the netural rate should be a level where the real overnight rate is a positive number. The implication being that in order to cool inflation, the Federal Reserve must raise the nominal overnight rate above the rate of inflation.

The Long Road to 2%

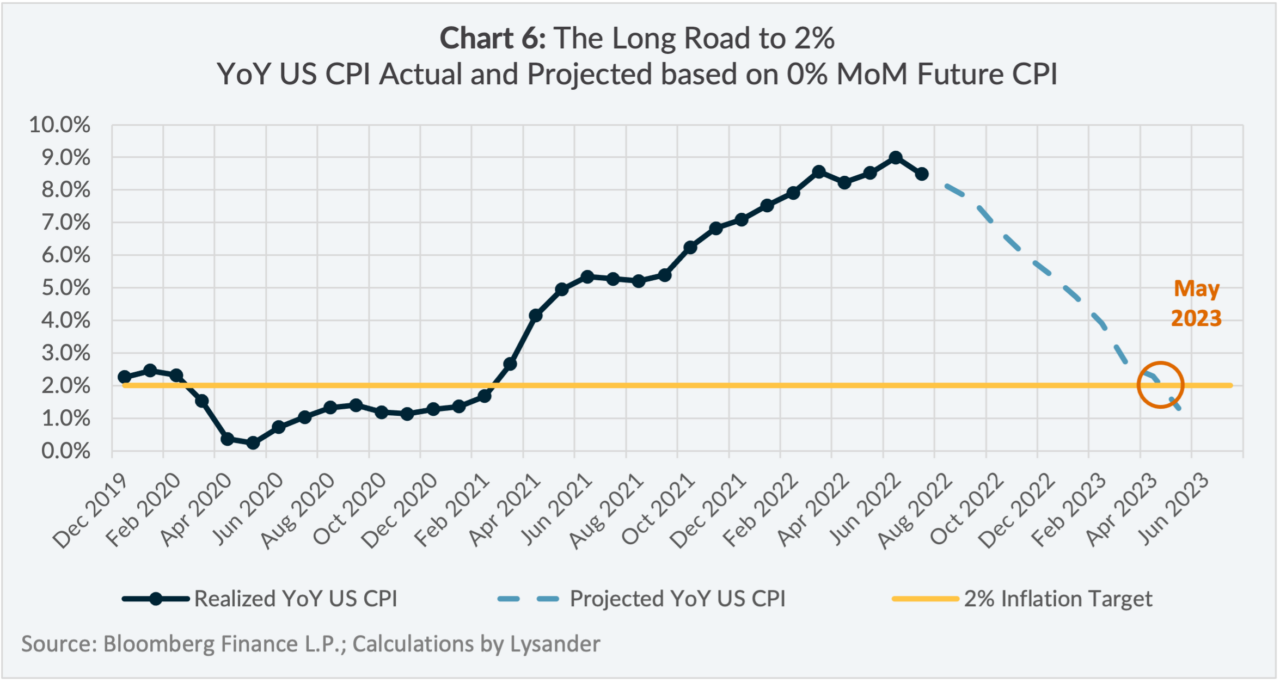

A core tenant of the bull-camp narrative is that inflation will naturally dissipate, and in the same vein there has been a lot of talk about YoY US CPI having “peaked”.

While there may be some truth to that – the 8.5% reading for YoY US CPI in July 2022 did come down from a reading of 9.1% in June 2022 – we are still a long way from stable inflation.

As illustrated in Chart 6, even if MoM US CPI were to be 0% in every consecutive month going forward, US CPI wouldn’t get below 2% until May 2023.

CONCLUSION

With US equities and bonds declining in tandem in 2022, many investors are likely confused and looking to the past for answers.

It could be tempting to establish a bull-camp narrative from the “Powell Pivot” of 2019 and apply it to what might happen in 2022. However, it must also be remembered that inflation is drastically higher than it was in 2019.

The Federal Reserve has committed to cooling inflation in 2022, which means we will likely see further increases to the overnight rate and possibly see it increase to the point where the overnight rate exceeds the rate of inflation – thus creating a positive real overnight rate.

Cooling inflation could take some time. There is usually a lag from the time monetary policy is implemented, to when its impact is reflected in the economic data. With inflation at already high levels, the journey back to 2% could be many months if not years.

For investors, these factors suggest markets sentiment could assume a bear-camp narrative tilt going forward, and further caution with their asset mix positioning could be warranted.

POSITIONING AT LYSANDER FUNDS

At Lysander Funds, we provide a suite of actively managed mutual funds in different asset classes including fixed income, preferred shares and equity. Our partner portfolio managers tend to follow bottom-up (company-first) approaches rather than top-down (macro-first) approaches.

We believe the current backdrop of uncertainty presents a unique opportunity for actively managed investment strategies to outperform passive. This is particularly true for fixed income, where passive investment strategies tend to have greater sensitivity to movements in term interest rates (i.e. high duration) and greater downside risk if term interest rates continue to increase.

Our fixed income portfolio managers are mitigating the risks posed by high inflation by lowering their exposure to interest rate risk (i.e. lower duration) and using judicious credit selection to achieve overall yields greater than their benchmarks.

For a list of our mutual funds, please visit www.lysanderfunds.com.