Not Sparing the Expens-ive

The powerful rally in risk assets in 2023 imbued 2024 with a continued enthusiasm for risk. That saw investors chasing returns at literally any cost or price. Patient or risk averse investors were left behind by those willing to just “Buy In” to the market momentum. The buying fever, if not euphoria, was supported by monetary easing by central banks and then the election win of soon to be President Trump.

Trump Pumped!!

Equities and corporate credit saw continued buying at very expensive historical levels. In the U.S., the staid and older economy Dow Jones Index was up a mere 12.9% for 2024. In comparison, the supercharger of AI dreaming (hallucination??) lifted the S&P 500 by 23.3% and the tech heavy NASDAQ by 28.6%. The S&P 500 saw its best 2-year performance since 1997-98 and the question on everyone’s mind is whether this sizzling performance can continue.

Incoming U.S. President Trump seems to have met with the stock market’s approval. Elon Musk has seen his fortune and fortunes soar on his support for Trump, regaining his title of the world’s richest person. Tesla’s stock was down 43% year-to-date in late April 2024 when the new First Buddy went all-in on his Trump bet. It’s up 188% since then, with a 60% return since Trump won the Presidential election. Clearly, this investor enthusiasm believes that whispering in Trump’s ear will be very profitable for Tesla and Mr. Musk.

Bonds were a different story. The Bloomberg Treasury Index ended the year with a mere 0.6% return, with the price depreciation from rising yields just offset by interest income. Long Treasury bonds were down 6.4% from rising yields over the year but Short Treasury bonds returned a decent 5.3% as their yields fell on Federal Reserve (Fed) easing. It was credit and corporate bonds that carried the day in the fixed income market, as risk premiums shrank and credit spreads narrowed substantially. The interest rate sensitive Bloomberg Corporate Bond Index returned 2.1% but the shorter term and much riskier Bloomberg U.S. Corporate High Yield Index was up 8.2%.

Trump Dumped?

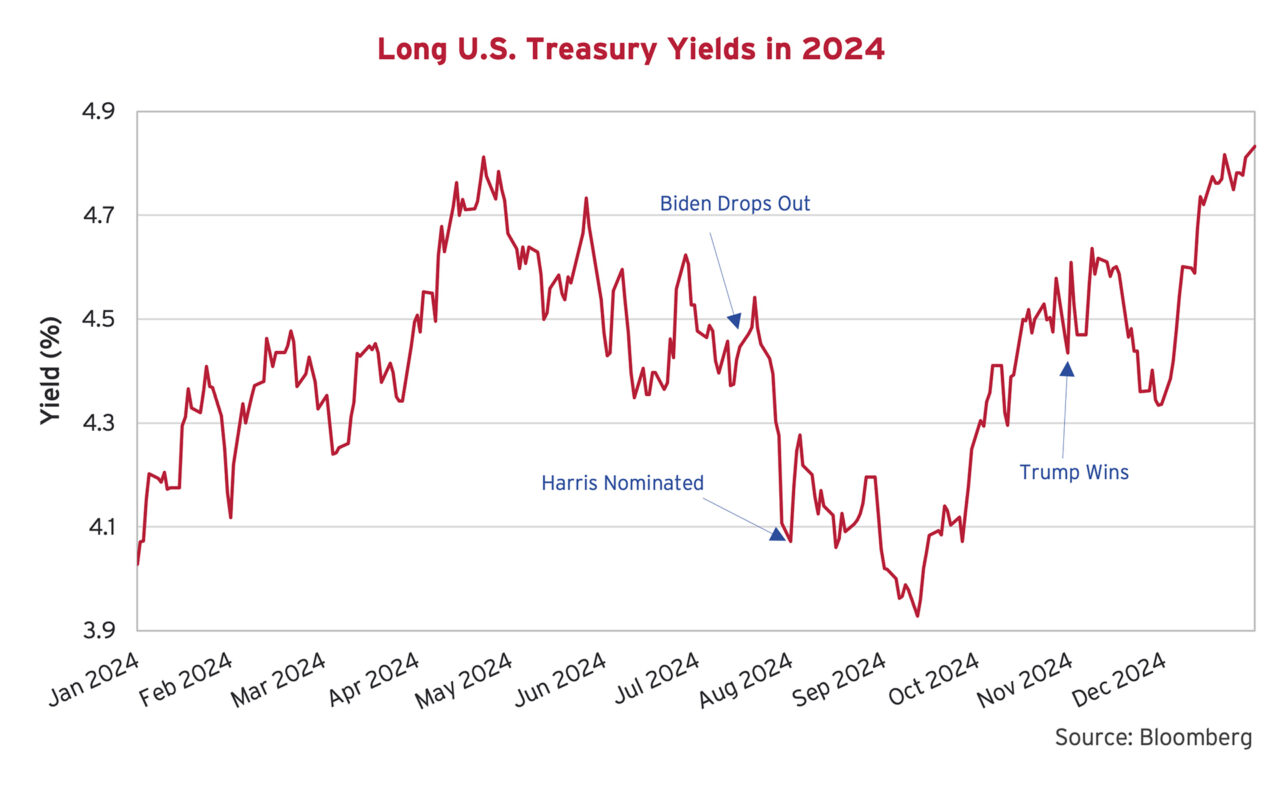

So, it was up, up and away in the financial markets, except for government bonds. Worries about the size of government deficits and continued U.S. economic strength keeping inflation “higher for longer” were accentuated with Trump’s election and his stated policies. The bond market is not as enthusiastic about Trump as the equity market, as can be seen in the chart below of long U.S. Treasury yields in 2024.

Long yields rose from just over 4% at year end 2023 to a peak of 4.8% in May on Joe Biden’s weak election prospects. When Biden dropped out on July 21st, yields began to fall and bottomed below 4% when it looked like Harris might win. As the election neared and Harris’ prospects faded, yields rose back up and peaked at 4.6% just after Trump’s election win. They fell on post-election optimism but soon started rising again to the current 4.8%, equalling the highs of early 2024.

Em Tu, Central Brute?

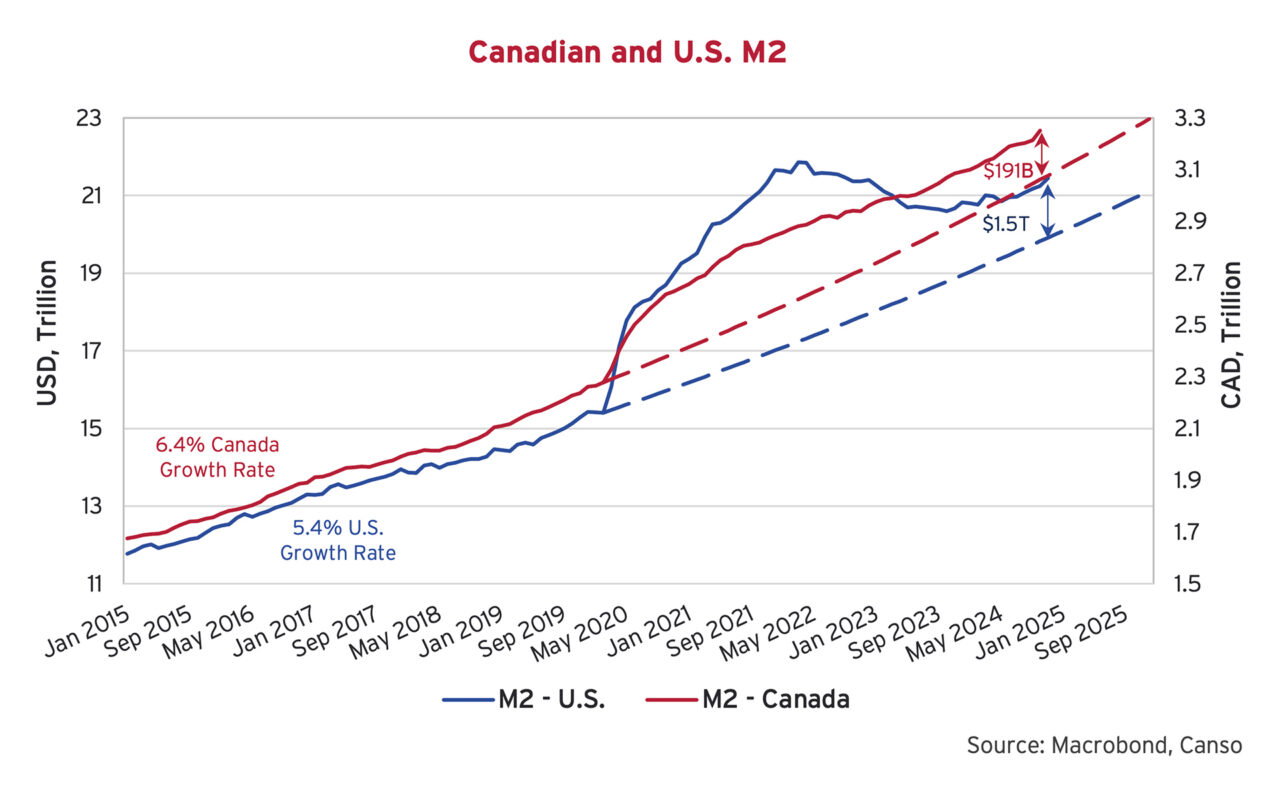

The real question is whether all the financial market enthusiasm will continue. The old market saw of “Don’t Fight the Fed” would seem to apply here. In our opinion, the vast amounts of money produced by central banks during their Covid hysteria continues to spill over into the investment markets. The huge increase in M2 money supply by global central banks certainly eased the economic pain from the Covid pandemic but it created excess money supply. The chart below, that we’ve shown you in previous editions, shows the increase in M2 in both the U.S. and Canada since the pandemic began. This was unprecedented in both countries and was well above what was necessary to support actual economic activity. As a monetarist economist would tell you, inflation needs expanding money supply, increasing above that needed by the actual economy. This applies to both consumer inflation and quite possibly to asset price inflation.

In the chart above we have plotted the growth rate of Canadian and U.S. M2 from December 2014 to present. Canadian M2 grew 6.4% and U.S. M2 grew at 5.4% annualized until the pandemic monetary stimulus began in April 2020. Canadian M2 then jumped from $2.2 to $2.8 trillion with that stimulus, an increase of 27% in less than a year before reverting to a more normal growth pattern. U.S. M2 growth was more pronounced, growing 40% from $16 to $22 trillion in just over a year, also far above its pre-pandemic growth rate. This gave the Canadian and U.S. governments the money they needed to stimulate their economies by issuing bonds and spending those funds. It also provided the money to support inflated prices for goods and services, as soon became clear.

A Graphic Monetary Tale

A graphic lesson in monetary policy implementation can clearly be seen in this chart. The Bank of Canada was more aggressive in tightening its bank rate but stopped earlier than the Fed, ceasing its increases and started lowering rates earlier. This can be seen in Canadian M2 which peaked and now is almost paralleling its growth rate prior to the pandemic as the Bank of Canada expanded money supply further. The U.S. Fed wasn’t as aggressive on easing rates and actually shrank M2 from $21.9 to $20.9 trillion to keep interest rates higher. The graph shows the major difference in growth rates with Canadian M2 continuing to grow to hold and then lower interest rates, and the U.S. actually shrinking M2 before resuming a more normal growth pattern, seeing it expand by $600 billion and now paralleling its pre-pandemic rate of increase. This has allowed the Fed to lower interest rates. As the chart shows, Canadian M2 is about $191 billion over where its pre-pandemic growth rate would have been, and U.S. is about $1.5 trillion.

We believe that current euphoria in risk assets in the U.S. and other financial markets reflects that huge increase in U.S., Canadian and other countries’ M2. All that money created needed to go somewhere. Normal consumers have spent much of the extra M2 increase they received in stimulus payments and wage increases on the higher prices they are now paying for goods and services. These have shown up in the 22.8% increase in the U.S. CPI since December 31st, 2019. Other more prosperous investors have money beyond that necessary to live on and have been putting that excess into the financial markets. Their obvious financial success begets envy and further investment as others are drawn into the markets, and leverage amplifies the uptrend.

Bubble Trouble??

Are we in an infamous “Financial Bubble”?? We’ll really never know until it’s over but a necessary precondition for a financial bubble is a substantial expansion of money supply and we have that in spades. Central bankers use “monetary ease” to improve the economy, and that’s what they are up to now. In traditional economic terms, the loosening of monetary policy expands money supply, creating more money in circulation to lower interest rates, the price of money. More money equals lower interest rates. More money also can mean higher inflation as the current Fed has learned from recent experience. Remember “transitory inflation”? Government deficit spending is rising and that also needs to be financed by an increase in money supply or government demand will “crowd out” private sector capital and raise bond yields.

The Sins of Our Monetary Fathers

Unless we are into a very rare “It’s Different This Time” moment, it means that the economies with loose monetary and fiscal policy will probably run hotter than predicted, possibly with higher inflation. For those of you thinking to yourselves that a recession would bring down inflation and interest rates, we often had recessions during higher inflation periods from the 1970s to the 1990s. The definition of recession is “negative real growth” and you can get there by having inflation higher than nominal growth i.e. 4% inflation and 3% nominal economic growth equals -1% real growth and you’re in recession. It’s hard to find an economist or market strategist these days that believes that higher inflation is a possibility. The consensus is that our recent high inflation was beaten for good by higher rates and tighter monetary policy and will not return. That was also the case in the mid 1970s when the economic consensus saw inflation and monetary policy “getting back to normal” after inflation fell for 2 years. Monetary ease meant that inflation reignited and “normal” inflation and monetary policy didn’t happen for a very long time.

An Eerily Similar Pattern

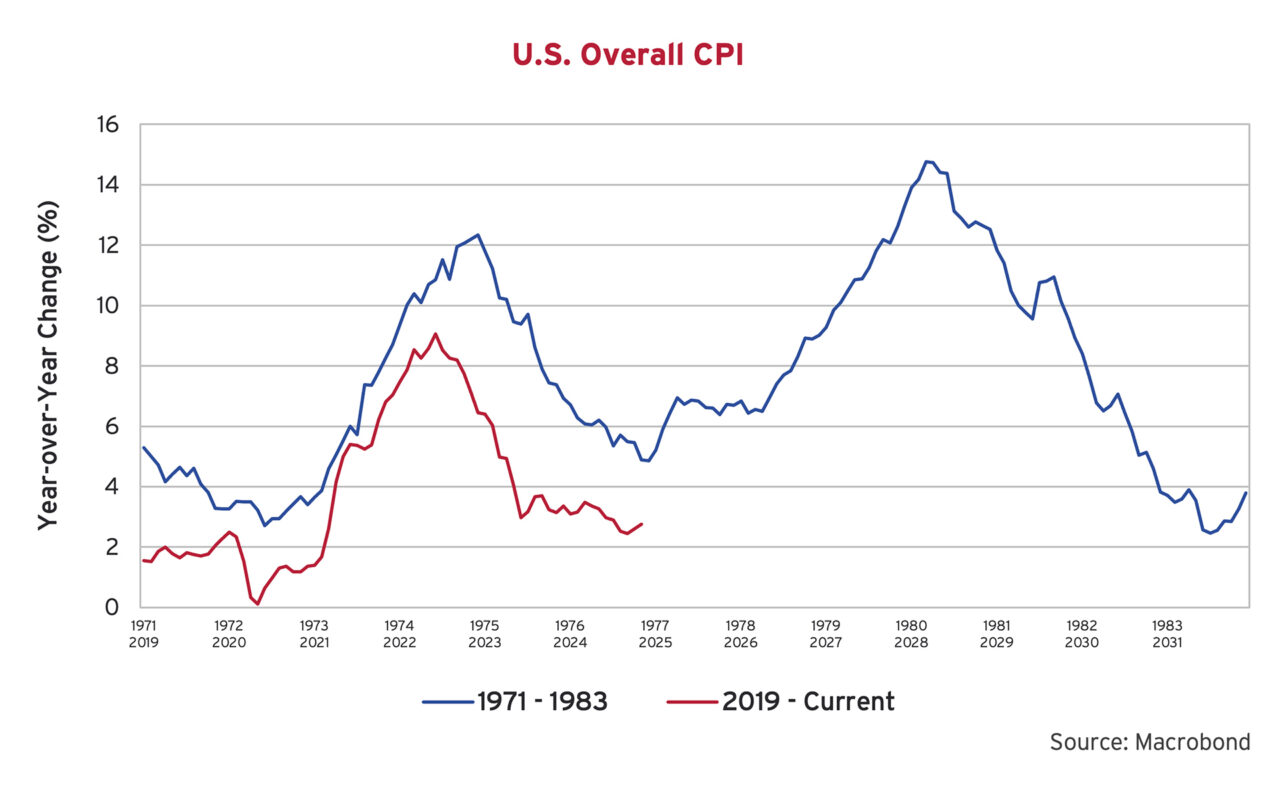

The chart above compares U.S. CPI in the period from 1971 to 1983 (blue line) to the current period starting in 2019 (red line). In the 1970s, U.S. CPI moved from 3.6% in early 1973 to above 12% in 1974 as monetary ease to fight the Arab Oil Embargo provided the fuel for higher inflation. The Fed’s monetary forefathers believed they had inflation under control when it fell from just under 12% in 1975 to 5% by the end of 1976. History is not necessarily the future, but subsequent easing soon saw ingrained inflation move up to above 14% before the Volcker Fed jacked interest rates up over 19% to bring it under control. The current situation is not all that different. The U.S. CPI has fallen from over 8% to under 3% in an eerily similar pattern. Today’s bond market currently is imbued with a similar optimism that we’re back to the 2% CPI future, and that very well might not be the case.

The “King of Debt” Regains His Throne

The U.S. now has an incoming Presidential Administration that is headed by Donald Trump, someone who has promised to both cut taxes and the deficit, while also promising to keep up spending. In Mr. Trump’s first term in office, he ran record peacetime deficits, even before the pandemic saw him spend even more. Trump is the self-styled “King of Debt” and looks to make the U.S. Treasury’s job of selling its debt more difficult. Trump also was the first President since Nixon to jawbone the Federal Reserve into lowering interest rates for no particular reason.

All politicians make promises that are soon broken, but Trump’s salesmanship took that to a whole new quantum in the past election. Continuation of the Trump tax cuts plus no taxes on social security, overtime wages, tips and his spending promises by incoming President Trump have been estimated by impartial budget analysts to add as much as $15 trillion to the U.S. deficit over the next 10 years. Considering the U.S. deficit for Fiscal 2024 ending September 30th was $1.8 trillion, an 8% increase over 2023, the stated Trump plans could almost double the annual deficit.

Beautiful Tariffs and Much Hyperbole

Mr. Trump has promised to replace the lost tax revenues with his “beautiful tariffs” on imports, but that begs the question of who will pay for the tariffs. If companies selling goods in the U.S. raise their prices to cover the tariff costs and domestic competitors follow suit, then there could be a serious upside for inflation. Trump has also promised to cut government programs to offset the tax revenue drop. That would probably hurt many of the low income voters that voted for him and betray his promised improvement to their lives.

What will happen when Trump’s promises and plans run into economic reality? There is so much hype in Trump’s platform that it is hard to predict anything, so we won’t even bother. Nobody really knows, including Mr. Trump and his incoming administration. Trump won on promises made to many different groups that are very often conflicted and at cross purposes. Trump’s promises boil down to “Make Everything Better Again” and that’s attractive to voters, but reality bites mightily into political rhetoric.

Wishful Policies

The professional Wall Street and business consensus is that Trump won’t implement his more radical ideas and policies, but we think there’s a lot of wishful thinking in that view. The financial chattering class is breathless in anticipation of an extension of the Trump tax cuts, lower corporate tax rates, crypto legitimization and less financial regulation. The tariffs on Mexico, Canada and China are posited as a salesman’s bluster or a politician’s promises to be easily broken. Allies are only allies when their interests coincide, so there are a lot of people within the Trump Make America Great Again (MAGA) coalition who are going to be very disappointed.

The many Americans who voted for Trump did so for vastly different reasons. Slapping huge tariffs on Chinese goods and ending Electric Vehicle subsidies is really not what Elon Musk and Tesla want but was and is a MAGA touchstone. The debate over highly skilled immigrant visas has already shown the cracks between the MAGA base and the tech billionaires who supported Trump financially in the election. The rejoinder from Vivek Ramaswamy that U.S. society values sports above technical skills so smarter foreigners need to be imported, is not a great MAGA marketing strategy. Implying Americans and their children are losers isn’t a winner with the union worker in Ohio who wanted to be great again and who voted for Trump. The Department of Government Efficiency (DOGE) has Ramaswamy and Musk taking aim at some very popular programs among Trump voters. Who or what will win? The question really is which of his policies and promises will actually be implemented and when.

Trussed In Me

We believe it depends on reaction of the U.S. financial markets to his plans, especially the U.S. Treasury market. As former U.K. Prime Minister (PM) Liz Truss, the shortest tenured PM in British history found out, it’s fine in the ivory towers of conservative thinking to postulate how things work, but when actual investors rebel against your plans and sell your bonds, then things change quickly. Truss was out and the unpopular Conservatives lost to Labour in the subsequent election. Keir Starmer of Labour became PM and quickly became one of the least popular in recent history.

Wealth Worshipping

Donald Trump is infamous for his disinterest in policy, but he hangs on the performance of the stock market and worships wealth. If a policy craters either the bond or stock market, we think he will be very quick to change course. He is notorious for discarding his close advisors. He demands loyalty but is quick to cut loose anyone who disagrees with him and/or hurts his personal prospects. The Federal Reserve will be challenged to implement sound policy in the face of strident Trump exhortations to lower rates. More money is always more popular than less, but the problem is that a large number of people who voted for Trump did so because they hate what inflation did to their finances. The Fed already has felt the scourge of higher inflation, but we doubt there’s another Paul Volcker waiting to defeat another bout when Powell’s term ends in 2026. The Fed “muddling through” could result in higher inflation and interest rates.

As China has found out with their residential real estate bust, non-financial asset prices are also inflated by loose monetary policy. The Fed has disappointed many in the financial markets by not immediately plunging interest rates to zero. We don’t think that after the recent inflation period that any central bank, except perhaps Venezuela, Turkey or Zimbabwe, is going to try a Zero Interest Rate Policy again. That means as the pandemic monetary stimulus runs its course that financial and other asset price appreciation could slow.

Trudeau’s Long Goodbye

In terms of Canada, the picture is even less clear. Forget the political drama with Justin Trudeau’s “Long Goodbye”, our economic housing addiction or the inflationary impact of a lower Canadian dollar. The threatened Trump tariffs are a mortal economic threat to Canada. Some Canadians are quick to dismiss the tariff threats as bluster, but those close to Trump say he believes they are actually great economic policy.

The Trump MAGA Republicans are not the free trade party of Ronald Reagan. They have more in common with the mercantilist tariffs policies of 1890 Tariff Act of William McKinley, as Trump himself frequently points out. It doesn’t matter that those were highly inflationary or if Trump truly understands what he wants to do. If there’s a trade war with the U.S., Canada would inevitably lose. U.S. exports to Canada are far less important to the U.S. economy than Canadian exports to the U.S. are to our economy. Placing an export tax on Canadian energy exports to the U.S., as some Canadian commentators have suggested, would not be popular with the Canadian energy producing provinces and would be a major provocation to President Trump who likes to be seen as winning. Probably the best Canada can do is to selectively hurt U.S. industries and key voters in their pocketbooks and try to outlast the chaos the tariffs cause.

Trump Chaos Redux

So, we’re going to have to wait to see what transpires when the new Trump Administration tries to translate its beliefs and policies into action. It’s not going to be a steady ship of state. Mr. Trump seems to think he should run his Administration like his former television reality show, The Apprentice. Factions compete for his attention and favour and try to outdo each other in “winning”. Losers need not apply. It’s up to him to build up his “contestants” or cast them out. All that’s guaranteed is that chaos and the unexpected will defy any attempts to forecast an outcome. Certainly, the drama just to re-elect a House of Representatives speaker suggests that Trump’s claimed massive election mandate might not be that strong.

Higher Risk Does Not Always Mean Higher Return

Rather than trying to predict economics and politics, we are concentrating on valuations, and they continue to look priced for perfection when our present situation is anything but. Uncertainty raises discount rates and lowers prices. The current investment vogue is to assume higher risk to juice returns. That makes us cautious with our client monies and, apart from some of our special situations, we think risk is currently underpriced with the current financial market enthusiasm and the many potential downsides that we see. We’re invested, but increasingly conservatively, focusing on things with better valuation metrics and avoiding higher risk situations. If we don’t understand a risk or we’re not paid to assume it, then we would rather wait for better opportunities.