In the first quarter of 2026, equity performance in North America diverged meaningfully. Through March 31, 2026, the S&P 500 Index was down 4.6%1 for the quarter, while the S&P/TSX Composite Total Return Index gained 3.3%2, extending the Canadian market’s quarterly winning streak to seven. The U.S. market was dragged lower by sharp declines in mega-cap technology stocks, while Canada’s S&P/TSX Composite Total Return Index benefited from its heavier exposure to financials, energy, and materials.

On the economic front, the U.S. economy entered 2026 in reasonable shape but faced increasing cross-currents. GDP growth had slowed to an annualized rate of 0.7%3 in the fourth quarter of 2025, though that figure was distorted by a government shutdown that subtracted 1.2 percentage points from growth; consumer spending grew at an annualized 2.0%4 and business fixed investment at 2.2%5, boosted by data center and AI-related capital expenditure. The unemployment rate stabilized at 4.4% as of February 2026, after having risen to 4.5%6 in November 2025.

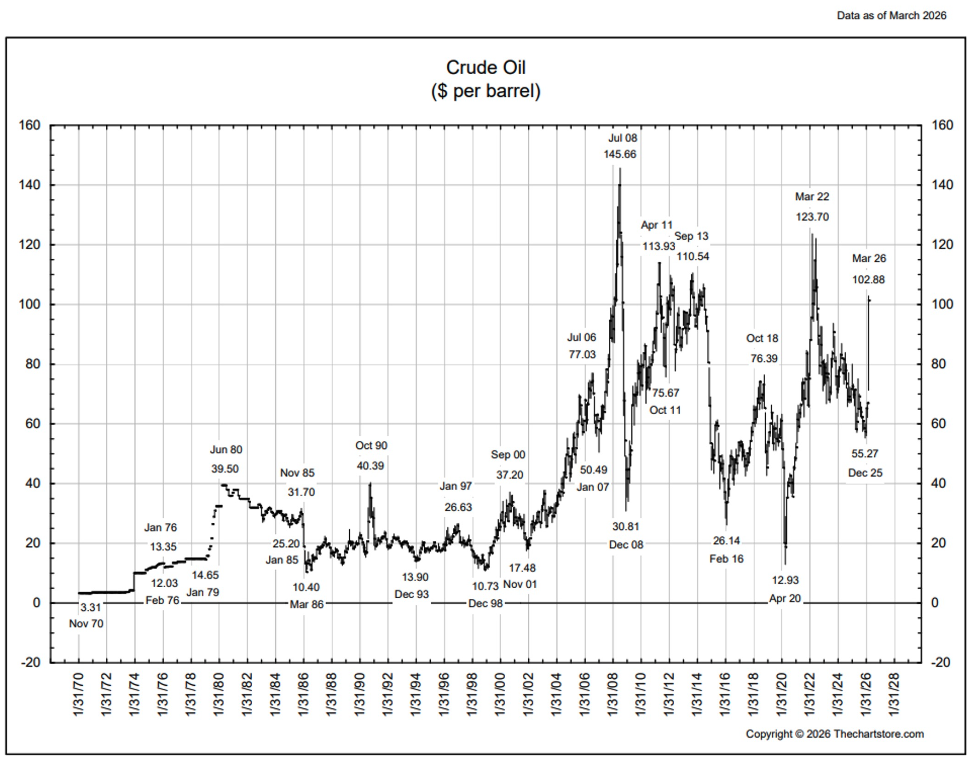

In Canada, economic conditions were softer, with the S&P Global Composite PMI recording 47.6 in March — a fifth consecutive month in contraction territory. Real GDP rose 0.1%7 in January and Statistics Canada’s flash estimate pointed to 0.2%8 growth in February, but more recent business surveys showed services activity contracting in March and manufacturing losing momentum. The Middle East conflict and trade tensions with the United States were major factors in Canada’s softening economy. Oil prices began the year at approximately US$60 per barrel but rose sharply in late February following the outbreak of the conflict involving Iran. Disruptions to the Strait of Hormuz and attacks on regional oil and gas infrastructure heightened supply concerns, pushing prices materially higher, as reflected in the chart below.

Since the United States and Israel commenced military operations against Iran, oil and equity markets have experienced elevated volatility, as investors reacted to rapid developments and ongoing official communications.

Lysander Patient Capital Equity Fund (the “Fund”) continues to be well positioned. As of March 31st, the Fund’s total portfolio yield was 4.5% and the portfolio’s overall characteristics continue to compare favorably to major indices such as the S&P 500 Index, and the S&P/TSX Composite Total Return Index. Relative performance versus the S&P 500 Index and S&P/TSX Composite Total Return Index in the first quarter of 2026 was positively impacted by a lack of exposure to mega-cap technology stocks, strong energy sector and financial sector performance and the realization of profits in some U.S. based holdings.

- S&P Global

- S&P Global

- Bureau of Economic Analysis

- Bureau of Economic Analysis

- Bureau of Economic Analysis

- Bureau of Labour Statistics

- Statistics Canada

- Statistics Canada